Ahead of the cotton sowing season in Punjab, there has been an increasing demand for Bollgard-3, a pest-resistant cotton variety which is yet to become available in India

Written by Anju Agnihotri Chaba | Jalandhar

March 3, 2025

In recent years, whiteflies and pink bollworms have wreaked havoc on the cotton crop in North India.

Cotton yields are down, as is the area under cotton cultivation — the crop was cultivated in only one lakh hectares in Punjab in 2024, down from nearly eight lakh hectares three decades back. The drop in acreage has in turn harmed the ginning industry — only 22 ginning units remain operational in Punjab today, down from 422 in 2004.

Ahead of the cotton sowing season, farmers are thus calling for the swift approval of Bollgard-3, a new pest-resistant genetically-modified (GM) cotton variety developed by Monsanto. Can this be a game-changer? The short answer is that it can be. But Indians won’t have access to it any time soon.

Bollgard-3, a Bt cotton variety

Bollgard-3 was developed by Monsanto more than a decade ago, and shows remarkable resistance to pests. It contains three Bt proteins Cry1Ac, Cry2Ab and Vip3A that cause insect death by disrupting their normal gut function. This in turn allows for the growth of a healthier cotton crop, and increases yield.

Bacillus thuringiensis (Bt) is a soil-dwelling bacterium with potent insecticidal properties. In the past few decades, researchers have successfully inserted certain genes from Bt in various crops, like cotton, providing these with insect-repellent properties.

Bollgard-1 was a Monsanto-developed Bt cotton introduced in India in 2002, followed by Bollgard-2 in 2006. The latter remains prevalent today.

And although these do have some pest-repellent properties, they are not effective against the whitefly and the pink bollworm, which arrived in Punjab in 2015-16 and 2018-19 respectively.

This is why farmers are demanding the introduction of Bollgard-3, which is particularly effective against lepidopteran pests like pink bollworm.

BG-2RRF, a more likely option

However, Bollgard-3 is not available in India at the moment, although it is being used in other cotton-growing countries around the world. What is the closer to being available is the Bollgard-2 Roundup Ready Flex (BG-2RRF) herbicide tolerant variety, although even this is pending final regulatory approval.

Dr Y G Prasad, director at ICAR’s Central Institute for Cotton Research in Nagpur, said: “Both government and private trials for BG-2RRF were conducted in India in 2012-13… But the application for commercial use is still pending with the government.”

Prasad said that BG-2RRF is an advanced seed technology that makes the cotton crop more tolerant to herbicides. This allows for farmers to better control weeds without harming the cotton plant, ultimately leading to better yields.

Bhagirath Choudhary, founder-director of the South Asia Biotechnology Centre (SABC) in Jodhpur, said that BG-2RRF could serve as a potential “gateway” for the development of next-generation seed technologies. He also said that the variety’s adoption could reduce risk of pest attacks by killing the weeds which host these pests, and by doing so, could make cotton farming more economically viable than it has been in the past few years.

“However, the approval of the technology has been significantly delayed due to regulatory hurdles, which have hindered the introduction of next-generation seed technologies,” Bhagirath said.

At the end of the day, even as farmers express their frustration regarding the pace of regulatory approvals, the fact of the matter is that farmers will have to make do with what they have, at least for the time being.

Dr Prasad said that adopting proper agronomic practices, such as proper seeding and mulching, can help increase cotton yields. Dr Bhagirath, on the other hand, pointed to methods such as high-density planting (sowing more plants in a unit area), and drip fertigation (which optimises water and fertiliser use). That said, pest management remains a challenge.

This is why Bhagwan Bansal, president of the Punjab Ginners’ Association, said that without high-yielding, pest-resistant varieties like Bollgard-3, the future of Punjab’s cotton industry remains uncertain. Many countries in the world are already adopting these (and even more advanced technologies) and reaping the rewards.

Atul Ganatra, president of the Cotton Association of India (CAI), said that Brazil is using Bollgard-5, a variety which protects against multiple pests, weeds, and insects. This has led to the South American country achieving astronomical yields of 2400 kg per hectare, compared to only 450 kg in India.

“In India, we are getting a profit margin of only 15%, and that too on a bumper harvest, with no pest attack. In Brazil, the profit margin is 85% of the input cost,” Ganatra said.

(Source: https://indianexpress.com)

Shurley: No Price Bump Seen from Lower Cotton Acres

By Dr. Don Shurley

March 3, 2025 (Source: www.cottongrower.com)

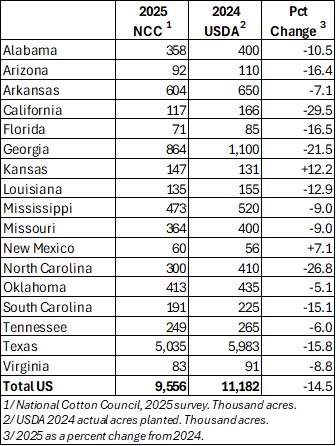

U.S. cotton acres planted are expected to drop 14.5% this year according to the National Cotton Council’s survey. If realized, this would be the lowest acreage since 2015 and the sixth lowest going back all the way to 1975. Yet last week (Feb. 28), cotton prices (nearby old crop May 2025 futures) dropped to 65 cents – the lowest in roughly five years. New crop December 2025 stands at roughly 68 cents.

At last week’s USDA Outlook Forum, cotton acres for this year were pegged at 10 million acres compared to the NCC 9.56 million. With either number, if we assume average abandonment and yield, we get a 2025 crop not much different (slightly smaller to just a little larger) than last year even with this reduction in acres planted. Perhaps this is one reason why the market has yet to show any upward price response to the prospect of lower acres.

The decline in cotton acres likely means an increase in corn, soybeans, grain sorghum, and peanut acres. Or perhaps it could also mean some acres may be left out of production this year. USDA’s Prospective Plantings report will be out on March 31.

Prices have been on a long slide since October. There was a recovery after the big drop back in November. Prices had shown a nice recovery in the past couple of weeks but moved weaker this past week and dropped all the way to 65 cents.

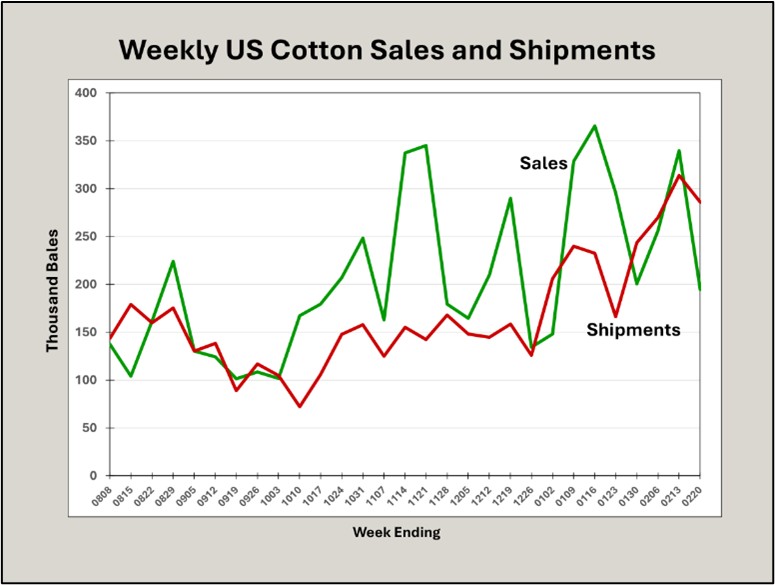

Export sales and shipments have been stronger over the past month – taken as a positive sign by the market and perhaps signaling that demand is improving. But, both sales and shipments were down sharply in the latest weekly report – perhaps a reason for the price decline this week.

The February monthly USDA supply/demand report was little changed from January. World demand/use was increased slightly, production in China was increased 1 million bales, and imports for China reduced 700,000 bales. U.S. exports for the 2024 crop marketing year were unchanged at 11 million bales. Brazil production was increased 100,000 bales but exports were unchanged.

(Source: www.cottongrower.com)

Ugly Price Picture as Cotton Moves to May Contract

By Dr. O.A. Cleveland

March 3, 2025 (Source: www.cottongrower.com)

Unfortunately, the cotton market performed as expected during the past week, with the new spot month May futures contract free falling to the expiring March contract lows and setting up another challenge of the 65-cent market low and a potential test of prices as low as 63 cents.

It remains an ugly price picture as the May contract did establish a new life of contract low – just as the recently expired Dec. 24 contract had done once it became the spot contract after the Oct. 24 expiry. The extremely poor demand situation cannot be over emphasized (although many wish I would just plain shut up with that comment). The 63-cent challenge is not as far-fetched when noting that market lows have been established with each futures contract expiration.

Since the 2024 harvest season, the New York ICE contract has moved some 11-12 cents lower and is not through falling just yet. The upside potential remains at 69 cents, but it will take an Olympic style performance to even reach close to that point. Most of the trading will likely fall within the three cent, 64-67 cent range.

It would be thrilling to write a positive analysis, but the cards are not in the deck, Nary one for old crop, that is. The market for new crop remains challenging, but there are a few ripples of market activity allowing for higher prices. There is a possibility that the new crop March and May contracts will turn very positive, but these comments will look only at the old crop.

U.S. weekly export sales remained well on target to reach the USDA export estimate. Net sales of upland totaled 166,900 bales. Even exports shipments were on target at 267,500 bales. However, recall this season’s export target is dreadfully low at 11 million bales and reflects USDA’s dismal demand estimate of only 11 million bales.

If we can be proud of reaching this target, de facto we are saying that the U.S. needs to produce only 11 million bales. Said another way, being happy with that number implies that one is happy with planted U.S. acreage falling to 5-6 million acres. That is not a misprint – five or six million acres. Certainly, one cannot be happy with that. Remember the word promotion.

The current pace of exports portends futures prices at 63-69 cents. Thus, there is little room for excitement with either the current pace of export sales or shipments. Even a rate of 10% or 15% higher than the current pace would still project only 67-73 cents.

The on-call situation for cotton continues to point to new contract lows in the May futures contract. On-call purchases dwarf on-call sales on the May contract. Of course, nearby on-call purchases have dwarfed nearby on-call sales all season.

It has only gotten worse – or rather more bearish. There is a flicker of light that July could hold more optimism, but only 2-3 cents more optimism. More likely, July futures are looking at the same 63-67 cent trading range.

Hearing the words bullish, bulls, increased spending, tariffs, and the positive words I would love to associate with cotton production, I scoff at the cotton’s industry refusal to understand that the world cotton trading pattern and the world marketing system has changed right in front of our eyes.

Too, each and every day the U.S. cotton industry seems to refuse to promote its sole product, and the situation will continue to sour. When broken, don’t continue to repeat the same thing that has been done for the past 50 years.

The market has changed, thus the approach to marketing and promotion must change. It truly is just as bad as we have said. Some in the industry have talked up the idea that consumer spending is lacking. Nothing could be further from the factual data.

The consumer has been the big engine driving the economy for four years now, although that strength is coming into question at present. Consumers, stressed as they are, still have funds. They are simply not buying cotton or cotton-rich goods and must be reintroduced to cotton.

I do not have a pretty picture. It is difficult to write such words. I am not happy and know you aren’t. Acreage estimates continue to fall for cotton. It is a shame that any increase in prices can come only if the U.S. grower reduces plantings.

And the double unwelcome news is this: if you reduce your acreage, others will increase theirs and you lose the economic ability to ever compete again. Give a gift of cotton today. ---

(Source: www.cottongrower.com)